Column By Mike Bibb

I’m not opposed to tipping someone for the efforts they expend when taking and delivering a food order at a local restaurant, or any other product requiring a delivery person.

Good, friendly service necessitates a reward.

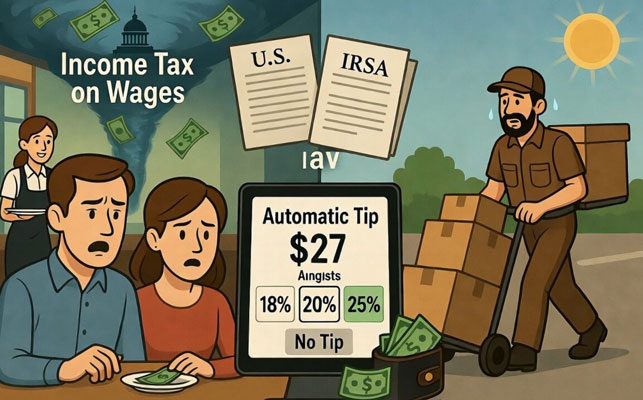

However, the amount of a tip should be decided by the customer, not automatically calculated by a handheld computer tablet and added to the bill.

For instance, the wife and I have dined at several establishments where, after the meal, the waitress scans our bank card and hands us a tablet to sign.

So far, nothing out of the ordinary.

Except, before signing, an array of tipping options appears on the screen as percentages of the total bill, not in dollar amounts.

For example, say the total for two meals was $27.46. A $3.00 tip would be about 11% of the original bill.

New total: $30.46.

However, the tablet’s tipping options begin around 18% of the bill and increase from there.

So, the $27.46 meal, with the computer-calculated tip, automatically escalates to a minimum of $32.40.

Representing a $4.94 tip for the same two meals.

Now, let’s consider the actual time and effort it took for the waitress/waiter to record and deliver the two-meal order — not including kitchen preparation time.

Does 7 minutes seem logical — 10, at the most?

A total order and delivery time of 10 minutes @ $4.94 would be $29.64 per hour (10 x 6 @ $4.94 = $29.64).

This amount exceeds the hourly wage a waitress/waiter receives.

Of course, the more expensive the order, the more expensive the requested tip, even though the actual order and delivery time may be nearly identical.

An equal reduction in meal price would result in a similar reduction in tip, but it is still 18% of whatever the bill’s amount.

Additionally, the waitress/waiter probably has multiple orders and deliveries going on at the same time.

An added benefit: tips — and overtime — are now supposed to be federally tax-exempt.

Before you grab the torches and pitchforks and come looking for me, keep in mind I retired from the package delivery business. Consequently, I know a little about pickup and delivery procedures, even though the products are different.

I didn’t wait tables and schlep Moons-Over-My-Hammy, green chili burros, mixed drinks, or hand Big Macs out a drive-through window.

Instead, I drove a brown delivery van about 180 miles a day, hand-carried or used a two-wheeled dolly (hand truck) to transport parcels from the van to homes and businesses in Graham and Greenlee counties.

Package weights ranged from 1 pound to 150 pounds. I performed this task for about 10-11 hours a day, at about 100 different locations.

Christmas season deliveries and packages increased considerably.

During my 25 years, I can’t recall a single monetary tip for my efforts. During Christmas, there were occasional goodies and treats that customers would hand me, but other than that, I had a few coins gifted to me in my pocket to contribute to a retirement fund.

Like the post office, drivers accepting tips may not be allowed, as it was never discussed.

The point is, tipping is a choice of the customer, not an expectation by the person performing the delivery task.

But since waitresses/waiters have traditionally received gratuities, they should continue to receive them, as I expect they are an important part of their earnings.

Which prompts me to wonder, if tips and overtime are now exempt from federal taxes, then why isn’t an individual’s regular wages and salary also exempt?

Why should eight hours of a workday be taxed when overtime and tips are not? Aren’t they all part of the same daily grind?

Wouldn’t it make just as much sense to tax only four hours, or two, or 30 minutes, or none?

Maybe, because our current income tax system is beyond comprehension. Originally, conceived and passed into law as a tax on company and corporate incomes (profits and gains), it has morphed into a discombobulated mess of rules and regulations of various descriptions and categories to such an extent an ordinary citizen working for a wage or salary is now held liable for payment of an “income tax” on that wage or salary, even though he/she has received no income.

Do you make millions of dollars and have the same tax advantages as General Motors, Microsoft, or Boeing Aircraft?

I doubt it.

Predictably, many of these mandates change every year, further confusing the situation. What was “taxable” one year may not be taxable the next.

Case in point: auto loan interest on a new car is deductible this year — but only if the vehicle is made in the U.S. Foreign-made cars and trucks, even if financed through U.S. banks and credit unions, are not eligible.

Thousands of IRS tax pages are incomprehensible, mumble-jumbled gibberish, and the procedures for complying are equally confusing, often requiring assistance from accountants, lawyers, and other tax “experts.”

What other Constitutional Amendment, besides the 16th, can change, flex, bend, be altered, dictated, ignored, and compelled to comply without Congressional approval and consent of three-fourths of the states? — (Art. 5, U.S. Constitution).

What other Constitutional Amendment can the President decide, through a bill, to suspend the collection of taxes on overtime and tips?

Then, if a different President and Congress take office, that tax suspension could be reversed by another bill.

Normally, modifications to a Constitutional Amendment are a complicated process, for the very purpose of preventing it from being changed at random based on a particular President’s opinion or the political party in control.

The only Constitutional Amendment to be repealed was the 18th (intoxicating liquors). The 21st Amendment restored a person’s right to legally enjoy a beer or a shot of Jim Beam.

As a result, if consuming beer, wine, and whiskey is legal again, then why is imposing an income tax on an individual’s personal wage or salary still required?

Remember, it’s called an “Income tax” for a reason. It is not labeled a “Wage and Salary tax” for an equally important reason: “No capitation, or other direct tax, shall be laid, unless in proportion to the census or enumeration herein to be taken.” — (Art. 1, Sec. 9, U.S. Constitution).

That clause in the Constitution has never been repealed or amended. It reads and means the same today as it did when it was ratified on Sept. 17, 1787.

The 16th Amendment (Income tax) wasn’t ratified until Feb. 3, 1913 — 126 years later.

Yet no one ever tells us the differences between the two Constitutional provisions, and they certainly aren’t discussed in school. Instead, we accept what we believe is the law — because that’s what we’ve been sold for over a hundred years — but are actually two different forms of law: One deals with matters of law, and the other with issues of equity (income taxes, for instance).

Why? Because the nation was changing from a primarily privately owned agrarian economy to an industrial one, with public corporations evolving into large employers of people to produce goods.

As a result, the government needed revenue to sustain its growth, but was limited by Constitutional restraints from taxing individuals directly.

Consequently, after several failed attempts, Congress finally devised a plan whereby the corporate arena would be required to pay a tax on the profits and gains of their business — the Income Tax came into existence.

Those profits and taxes are simply factored into the product’s price and passed on to the consumer. Since the taxes would be imposed equally on everyone purchasing the product, there are no varying scales that favor one consumer over another. Also, the consumer can avoid the taxes by not purchasing the product.

The income tax was never intended to be a tax on individuals working for a corporation, and no Constitutional Amendment has ever been enacted to permit such a tax on workers.

However, for various reasons, including Congressional and Judicial neglect (or, maybe on purpose), an income tax is now imposed on virtually anyone who has received any form of remuneration or compensation for his/her labor — despite having no gain or profit. Simply working for an agreed-upon wage to perform a specific job is not a taxable capital gain or profit event.

At least, I don’t believe it is. A person has the right to be paid for his work without the government grabbing a big chunk of it in the name of “Income taxes.”

Additionally, where is it written in the tax code that an individual who earns a wage or salary is required by law to file tax forms and pay taxes on that income?

Realistically, it appears the word “income” in income tax is now construed as meaning any form of money, gift, wage, salary, bonus, gambling winnings, betting, inheritance, and anything the IRS may consider as earned income.

Obviously, we’ve strayed far from the original intent of the 16th Amendment, and any efforts to correct the problem doesn’t seem to be of high Congressional priority.

Understandably, government’s addiction to your money is like a Los Angeles methhead insisting he needs the cash for a new set of false teeth to replace the ones that rotted out.

The excuses never end.

Besides, when we’re already supporting a country that is nearly $40 trillion in debt, does collecting income taxes really make any difference?

Our leaders are spending, printing, and borrowing money faster than it can be collected. In addition to the big federal and state departments of government, money is routinely handed out to other four-, five-, and six-letter agencies that no one has ever heard of. As a result, the more the IRS takes from us, the further behind we get.

However, if you balk at “Paying your fair share” to keep this nonsense rolling, it makes tax officials mad. As if they think you are robbing them of something the government has already taken from you.

If you’re lucky and receive a tax refund, keep in mind you are only getting some of your own money back — without interest.

In the meantime, millions of folks don’t pay any income tax at all. Billions and billions of your tax dollars are routinely handed over to fraudulent schemes by the very agencies you’ve entrusted to disburse your money fairly and lawfully.

Can’t make this stuff up. We’re being fleeced by a taxing authority that has no idea where all the money it collects goes.

And, obviously, don’t care as long as they can pick your pockets for more.

Perhaps, next week, President Trump will announce “No tax on wages and salaries.”

That would send career bureaucrats, tax collectors, liberal judges, and fraudsters into uncontrollable fits of rage — psych wards would fill up before noon.

Unless, of course, you happened to be the drug addicted, fortunate son of a former U.S. President who was pardoned for his multi-million-dollar income tax violations and convictions.

Sometimes, it’s handy to have a daddy in high places with an autopen — even if he has difficulty finding the White House, remembering his son’s name, and believes he should still be President.

Incidentally, I welcome anyone’s contrasting opinions on the validity of the income tax as it relates to an individual’s personal wages and salary.

Maybe I’m mistaken in what I believe. Maybe I’m emitting more methane than a Christmas turkey. Maybe my brain synapses are misfiring. Maybe I’m just an elderly man with a poor memory.

Maybe, none of the above. . .